Accrual accounting is a form of accounting in which income and costs are recorded when a transaction happens rather than when a payment is received or paid. The matching principle states that income and costs should be recorded at the same time.

DIFFERENCE BETWEEN CASH AND ACCRUAL ACCOUNTING

- Revenue and costs are recognized and recorded as they occur under accrual accounting, but cash basis accounting does not capture these line items until cash crosses hands.

- Although cash basis accounting is more straightforward, accrual accounting provides a more realistic picture of a company’s health by considering accounts due and receivable.

- Because it smooths out results over time, the accrual technique is the most widely utilized approach, particularly by publicly listed firms.

IS ACCRUAL A DEBIT OR CREDIT

An accrual journal entry is often a debit to an Expense account. Your expenditures will rise as a result of the debit entry. Credit is also applied to an Accrued Liabilities account. Your obligations grow as a result of the credit.

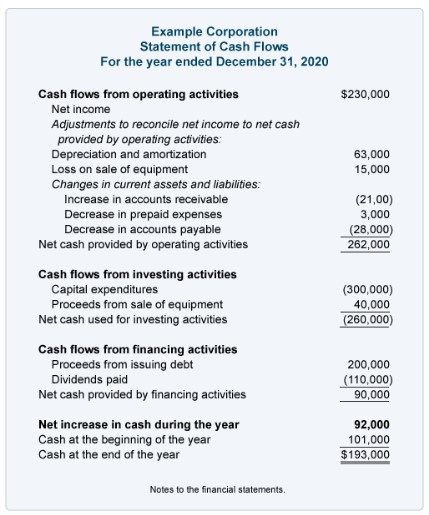

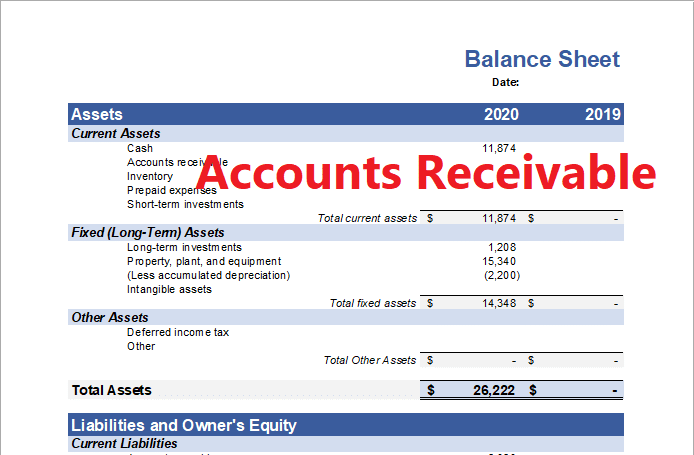

read More about Balance Sheet

WHO MUST USE ACCRUAL BASIS OF ACCOUNTING

- If a company’s average gross receipts over three years exceed $26 million, it must use the accrual method of accounting.

- There are more reasons why your startup may need to utilize this technique sooner or later. Publicly traded companies, for example, must adhere to the Generally Accepted Accounting Principles (GAAP). While GAAP is not a law, it is a set of guidelines for managing finances and disseminating financial reports. GAAP standards demand accrual-basis accounting. If you’re unsure whether GAAP applies to you, consult a certified public accountant (CPA) or an accounting firm.

DISADVANTAGES OF ACCRUAL ACCOUNTING:

Accrual accounting is more complex, necessitating more time and resources, which most small business owners do not have. It includes keeping track of cash flow, accounts receivable, and accounts payable.

It can also distort your company’s short-term financial picture. If you invoice $15,000 in a month, the accrual method will reflect that you earned the entire amount, even if you get nothing. Your books would reflect that you had more money than you have, which may interfere with paying bills or, worse, salaries.

read More about income statement

ACCRUAL BASIS OF ACCOUNTING EXAMPLE

Assume an appliance store offers a refrigerator on credit to a consumer. Depending on the conditions of the business’s agreement with the client, it might be months or years before the store gets complete payment from the customer for the refrigerator. Using the accrual accounting technique, the business will record the accrued income from the sale as soon as the refrigerator leaves the store, rather than at a later date.

HOW TO CALCULATE PROFIT AND LOSS IN ACCRUALS IN ACCOUNTING

When services are acquired or used and a bill is received from the vendor, expenses are incurred. Expenses are recognized under the accrual approach even if they have not yet been paid.

Subtract your accumulated costs from your accrued income. Under the accrual approach, the result is the net profit or loss.

Read more about how to calculate accumulated depreciation