The balance sheet is among the key three financial statements (income statement and cash flow statement) which the organizations prepare for reporting the financial information.

This statement is also called a statement of financial position. Balance sheets provide information regarding the financial position of any business.

Corporations or businesses require a balance sheet for the purpose of financial decision-making and for attracting investment in the businesses.

see also consolidated financial statements

Without an accurate balance sheet not only the reputation of the business will decline but also the business will unable to attract good investment.

Significance of Balance sheet for Businesses

The balance sheet provides information regarding the financial status of the business. Through this statement, the stakeholders can analyze whether the corporation is experience growth or decline.

The balance sheet includes all the information about the company’s assets and liabilities. If the business is experiencing growth then the balance sheet will show an increase in assets and liabilities however if the business is declining then its assets & liabilities will show a decline.

This statement should be prepared according to the Accounting Standards that are set by accounting regulatory bodies. IFRS and GAAP have provided the rules & regulations for preparing the balance sheet.

The balance sheet is considered among the most important financial documents of the business. The top management of any business take decisions after evaluating the balance sheet of the business.

With the help of balance, anyone can evaluate how much equity the business has issued or how much debt (Both Long-term debts and short term debts) the business has taken.

Not only the capital structure of the business can be evaluated with the help of a balance sheet but also the business can evaluate how many assets the business has acquired over a specific period (annual year or fiscal year).

Overall it can be said that the balance has huge significance for decision-making purposes and for providing detail financial analysis information to the stakeholders of the corporations.

Components of Balance sheet

The balance sheet mainly consists of two major parts which include the asset side and liability side. The assets and liabilities are then further divided into current and long-term items (noncurrent liabilities).

Assets

The assets side of the balance sheet includes information about the assets which the organization possesses. There are two types of assets that the organization possesses one is current assets and the other are fixed assets.

Current Assets

- Current assets are those assets that the organization used for their day to day operations.

- The current assets can be converted into cash within the period of one year.

- The current assets are utilized for performing routine business activities.

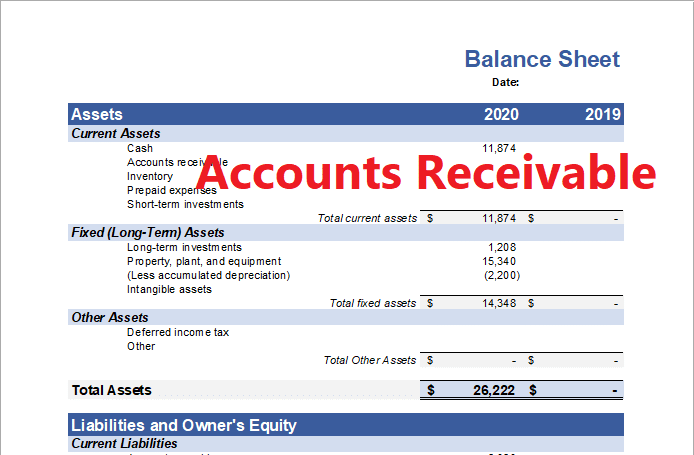

The example of current assets includes cash in hand, prepaid expenses, marketable securities, inventory, account receivable, etc. Usually, the corporations maintain their current assets in such a way that they can pay their short-term loans efficiently.

Fixed Assets

The fixed assets of the businesses include property, plant, and equipment PP&E, long-term investments, goodwill, intangible assets, etc.

As current assets have short life fixed assets have a long term lifespan. Fixed assets have a lifespan of more than one year that’s why they are known as fixed assets. After the completion of useful life, the business has the option to sell the fixed assets and purchase the new ones.

Usually expanding businesses show an increase in the assets of the businesses because the businesses keep on buying new assets so that growing business needs can be fulfilled. The growing assets indicate the strong financial status of any business.

Liabilities

The liabilities section of the business provides information about the current liabilities and long-term liabilities. The liabilities are the obligations which the business or any company have to pay to creditors.

Current liabilities

- The current liabilities are short-term obligations that have to be paid to the creditors within one year period.

- The current liabilities include account payable, short-term loans, deferred revenues, etc.

Long-term liabilities

On the other hand long term liabilities have a time period of more than one year. Long-term liabilities include long-term investments, notes payable, bonds payable, etc.

The shareholder’s equity

The shareholder’s equity section is also part of the liability section that provides information about the equity that has been issued by any organization include below accounts:

- Capital Paid.

- Retained earnings.

- Provisions

Example of balance sheet

Below is the example of a balance sheet: