Chart of Accounts definition

- A chart of accounts (COA) Also known as Accounts tree is a financial management tool that lists every account in a company’s general ledger, split down into subcategories.

- It’s used to keep track of a company’s finances and provide investors and shareholders with a better understanding of its financial health.

- Each chart of accounts generally has a name, a brief description, and an identifying code to make it simpler for readers to locate individual accounts.

CHART OF ACCOUNTS DEBIT AND CREDIT

To ensure that a company’s books are balanced, debits and credits are utilized in the accounting process. It increases the asset or expenditure accounts while decreasing the income or equity accounts when a debit is applied to those duplicate accounts. Credits work the other way around. To correctly record a transaction, each debit entry must have an equal and opposite credit input.

- Bookkeeping entries such as debits and credits balance each other out. Just keep in mind that every transaction must be accounted for by exchanging the same amount of money for another.

- The simplest way to understand this is to think about how a debit entry always adds one to the total and how a credit input always subtracts one (even though positives and negatives are not used in the actual journal entries).

- A debit is always placed on the left side of an entry for placement purposes (see chart below). It is possible to think of debit as credit since it raises asset or cost accounts while decreasing liabilities.

- An entry’s credit will always be on the right side. It increases liability, revenue, or equity accounts while decreasing assets, accounts, and accounts.

PURPOSE OF THE CHART OF ACCOUNTS

Companies use a chart of accounts (COA) to keep track of their finances and provide investors and shareholders with a better understanding of their overall financial position. It’s easier to keep financial statements compliant with reporting requirements if expenses, revenue, assets, and liabilities are all separate. The accounts owned by a corporation are generally listed in the order in which they appear in its financial statements. That implies assets, liabilities, and shareholders’ equity is shown first on the balance sheet, followed by revenues and costs on the income statement. These sub-accounts under the assets account could be included in COAs for a small business:

- Cash

- account for accumulating savings

- Balance of petty Cash

- Receivable accounts

- Funds that have not yet been deposited

- Assets in storage

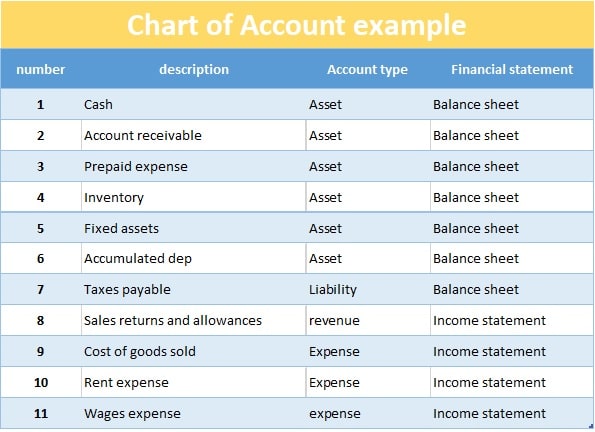

Example:

numberdescriptionAccount type Financial statement :

| Chart of Account example | |||

| Cash | Asset | Balance sheet | |

| Account receivable and debt Allowance | Asset | Balance sheet | |

| Prepaid expense | Asset | Balance sheet | |

| Inventory | Asset | Balance sheet | |

| Fixed assets | Asset | Balance sheet | |

| Accumulated depreciation | Asset | Balance sheet | |

| Taxes payable | Liability | Balance sheet | |

| Sales returns and allowances | revenue | Income statement | |

| Cost of goods sold | Expense | Income statement | |

| Rent expense | Expense | Income statement | |

| Wages expense | expense | Income statement | |