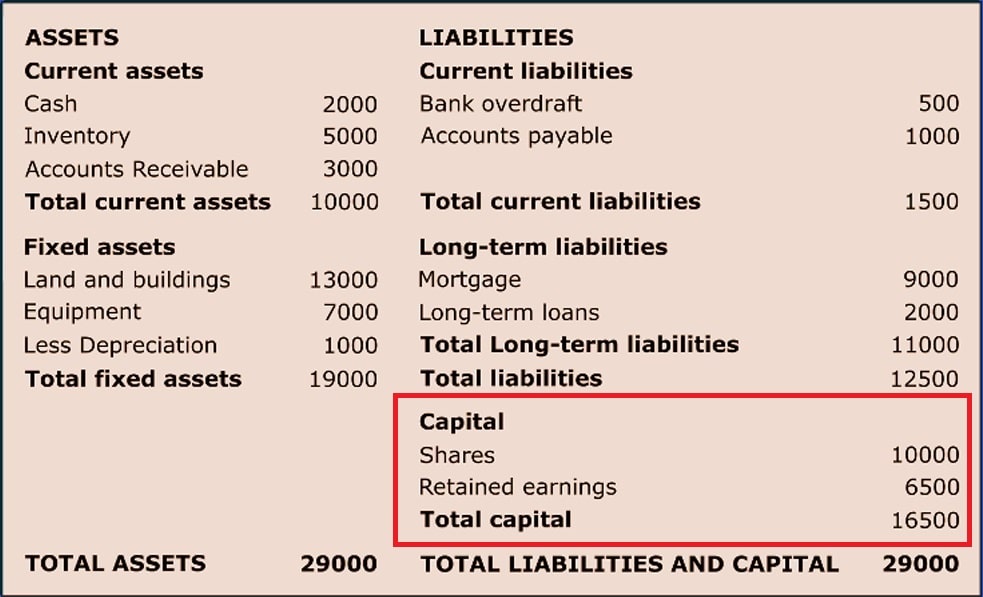

A company’s share capital is the money it raises by issuing regular or preferred stock. With other public offerings, a company’s share capital or equity financing may alter over time. It refers to the total money raised by the corporation through share sales.

SHARE CAPITAL IN BALANCE SHEET

A company’s share capital is disclosed on its balance sheet under the shareholder’s equity column. Depending on the source of the funding, the information may be reported in different line items. A line for common stock, another for preferred stock, and a third for additional paid-in capital are frequently included.

PREFERENCE SHARE CAPITAL

Preference shares offer the holder a fixed dividend, the payment of which takes precedence over ordinary share payouts. The capital raised through the issuance of preference shares is referred to as preference share capital. As a result, preference shares share some characteristics of both equity and debentures.

ISSUED SHARE CAPITAL

The monetary worth of the shares of stock that a corporation offers for sale to investors is issued share capital. The number of issued shares is usually proportional to the subscribed share capital, but neither figure can exceed the allowed amount.

PAID-UP CAPITAL

Paid-up capital is the amount of money received by a corporation from shareholders in exchange for equity shares. Paid-up capital is formed when a firm sells its shares directly to investors on the primary market, typically through an initial public offering (IPO). When investors buy and sell shares on the secondary market, no extra paid-up capital is created because the proceeds go to the selling shareholders rather than the issuing business.