What Do we Mean By Classified Balance Sheet

There are several types of balance sheets, but the most common is the categorized balance sheet. Providing information in a large number of line items may make it more difficult to read and find what you need. It also gives customers additional knowledge about the business and what it does in the market place. The solvency and leverage of a company can be determined by comparing current assets and liabilities, which can be done by investors and creditors. You may easily divide your balance sheet into two sections: current and long-term.

A balance sheet can include any number of subcategories or formats, but the following are some of the most common:

- Currently held assets

- Long-term financial investments

- Invested capital (or property, plant and equipment)

- Intangible property

- Liabilities in the present

- Long-term obligations

- The equity of shareholders

- Other resources

What Is The Difference Between A Balance Sheet And A Classified Balance Sheet?

An unclassified balance sheet includes asset, liability, and equity balances much like a classified balance sheet, however an unclassified balance sheet does not categorise the amounts; instead, it just lists them in their respective categories as they are. They are commonly used for informative reasons by small enterprises or individuals. Unclassified and classified balance sheets have different formats, but classified balance sheets are made to show specific information.

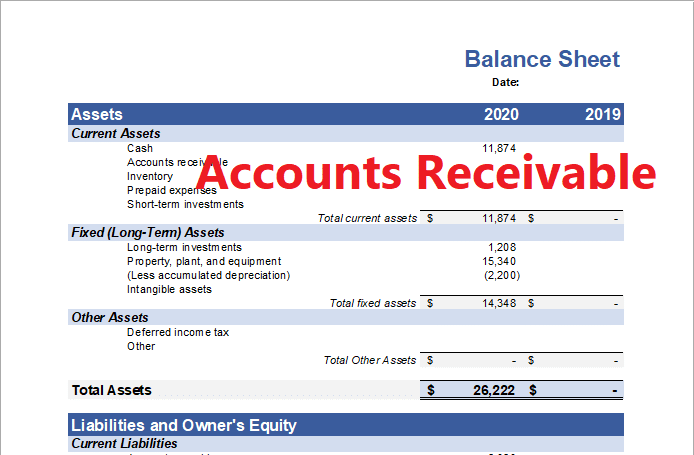

Equipment and fixtures, for example, are recorded under assets in the amount on the balance sheet above. Rather of being included in the asset list, furniture and equipment are reported individually under the fixed asset category. In order to make educated investment or loan approval choices, outside investors and creditors rely on a categorised balance sheet.

Know More Also About Income Statement

How Is A Classified Balance Sheet Organized?

One can discover changes in the asset mix over time by classifying assets, and then compare a company’s assets to the assets of a competitor or the industry average.

Liabilities will be divided into two categories if we divide our assets into short-term and long-term groupings. Liabilities that are expected to be paid off in the next year or operating cycle are known as current liabilities.

Current liabilities include things like accounts payable, accrued costs, client deposits, short-term notes payable, and the current component of long-term debt. This final division is vital. There are a great number of long-term commitments that need payment on a monthly or even weekly basis, such as mortgages.

Present-year commitments are those due in the next year, including the principal payments due in the following year. The interest component of such payments, on the other hand, is a cost in the period in which it is due.