Statement Of Financial Position Definition

The balance sheet is often known as a statement of financial status. The message summarises an organization’s assets, liabilities, and equity as of the report date. The information on the financial position can be used for various economic analyses, such as comparing debt to equity or current assets to current liabilities. Because it is one of the financial statements, it is frequently shown alongside the income statement and statement of cash flows.

Statement Of Financial Position Vs Balance Sheet

Many people believe that the balance sheet and the statement of financial position are the same things. However, there are several distinctions between the balance sheet and the idea of financial status.

The balance sheet and the statement of financial position are financial statements that provide an overview of the organization’s assets, liabilities, capital, revenue, and costs.

After each accounting period, companies create financial statements to gain a clear picture of how resources were used to enhance profitability over the fiscal year.

The balance sheet, in particular, is an essential financial statement since it displays changes in the assets, liabilities, and capital of the firm. The article that follows discusses both financial statements in detail and the similarities and differences between a balance sheet and a view of financial position.

Statement Of Financial Position Elements

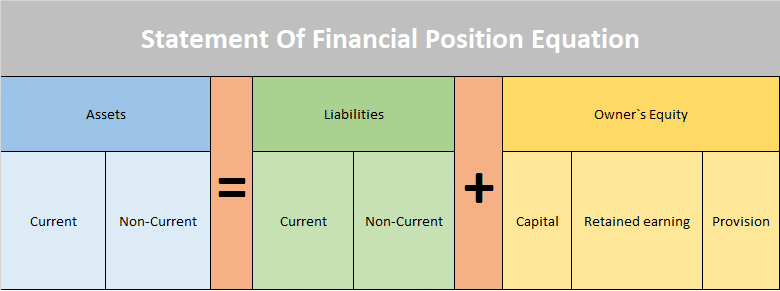

A statement of financial situation contains numerous essential items. Assets, liabilities, working capital (net current assets), and capital employed are examples of these. In general, assets are items that a company owns, whereas liabilities are goods or money that a company owes.

Assets are classified into two types:

- Current Assets

- and fixed (or non-current)

- Existing assets are short-term in nature; they will be owned for less than a year. Stock, raw resources, and currency are examples of such items.

- Fixed (non-current) assets are long-term because they will be owned for longer than a year. Vehicles, equipment, and structures are examples of such items.

Liabilities are further divided into two types:

- Current Liabilities.

- and long-term (or non-current)

Current liabilities, often known as short-term debts, are obligations owed by a firm that must be repaid within a year, such as an overdraft, trade credit, or a short-term business loan.

Long-term (non-current) obligations are loans paid back over more than a year, such as mortgages or long-term bank loans.

Working capital and net current assets are the same things. Current liabilities are subtracted from existing assets to arrive at this figure. Net existing assets are the funds accessible for day-to-day operations, such as paying salaries and acquiring shares.

Net assets are simply the monetary value of a company. This is computed by putting together fixed assets and net current assets (working capital). It may alternatively be calculated as the sum of total assets minus total liabilities.

The amount of capital used is calculated by adding equity and reserves to the long-term obligations, such as shareholder money. To create the balance sheet, this amount should always equal the net assets figure.

Statement Of Financial Position Equation

The financial status statement is prepared in the manner of the accounting equation:

Assets = Liabilities + owner Equity

check more here