prepayment expenses definition

Prepaid expenditures are those that have been paid in advance for future costs. In other words, prepaid expenses are those expenses that have been paid but not yet consumed or expired. According to standard accounting practices, the number of prepaid expenses used within one year is recorded on a company’s balance sheet. As the amount is deducted from the existing asset, the amount deducted is recorded as an expenditure on the income statement.

For example, a typical prepaid expense is the six-month insurance premium for a company’s cars, paid in advance. Prepaid Insurance is often represented as a current asset in the recent asset statement. If the business publishes monthly financial reports, the insurance expense will appear on the income statement as one-sixth of the six-month premium. Prepaid Insurance will have a balance equal to the amount remaining prepaid as of the balance sheet date.

prepayment journal entries

Prepaid rent’s first journal entry is a debit to prepaid rent and cash credit. These are both asset accounts that do not affect a company’s balance sheet in any way. The prepaid expenses are considered an asset since they offer the business future economic advantages.

How is prepayment appears in balance sheet

A buyer records a prepayment as an asset, whereas the seller records it as a liability. These things are often classified as current assets and current liabilities on each party’s balance sheet since they are typically resolved within a year.

While prepaid expenditures are initially capitalized as assets, their value is expensed onto the income statement over time. After the assets’ advantages are realized over time, the remaining balance is reported as an expenditure.

is prepayment current assets?

The current asset classification is necessary since most prepaid assets are consumed within a few months after their first recording. If a prepaid expense is unlikely to be used within the following year, it is categorized as a long-term asset.

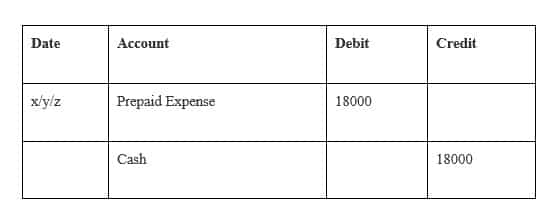

example of prepayment journal entry

You pay $ 8,000 in advance for six months’ rent. You paid for the space but have not yet used it. As a result, the sum must be recorded as a prepaid expense. To begin, debit the Prepaid Expense account to reflect an asset rise. Additionally, credit the Monetary account to remember the Cash lost.

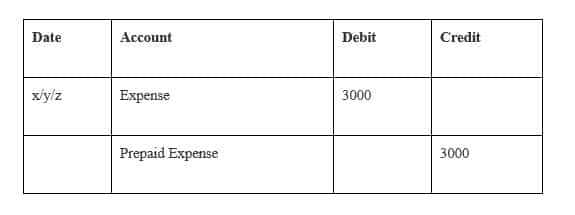

Adjust the accounts monthly based on the amount of rent used. Divide the entire amount by six ($ 8,000 / 6) since the prepayment is for six months. Each month, make a $3000 adjustment to your accounts.

Charge $3000 of the rent on a debit card. Credit the Prepaid Expense account. Each month, repeat the procedure until the rent is paid and the asset account is depleted.

check more here